One of the hardest things about investing your money is deciding who to listen to for advice. There’s a myriad of financial advice-givers out there, both paid and free, and fueled by the internet it’s really easy to find them all.

There’s a lot of roadblocks for people getting started in investing. They include things like…

- Not having much money, so not wanting to lose any money.

- Not knowing where to start.

- A retirement plan at work that isn’t flexible.

- Not coming from a family that invested.

All of those were true for me. But when I was in my early 20’s I got offered a job that came with a 401k. And while I didn’t know much about investing I knew that if my company was going to 100% match my investments up to 5% so getting that match meant I got 100% return on my investment from day one and that was pretty dang good. (Never say no to free money!)

And that’s how I got started. Then, after I left that first job, I’ve always had a Rollover IRA to manage which forced me to figure out how I wanted to invest that money.

Since then I’ve had great years and good years. But I’ve never had a year where my investments actually lost money. And over time I moved from mostly mutual funds into where I’m at now, a pretty good balance of company stocks and Exchange Traded Funds (EFTs) that perform in a way I feel comfortable with. I’m not beating the market but I’m surely beating the measly returns of a bank savings account.

The Most Important Thing is To Get Started

There’s no other way to say it. If you want your investments to work for you than you need to start building them up as soon as possible.

Think about it like this. If you’re in your 20’s and you have a job, let’s say at Starbucks. You are exchanging your time each week to receive a paycheck. To earn $25,000 you are exchanging 1,666 hours of your time in that year.

Exchanging time for money is limited because you have a finite amount of time. So if you need to make more money your only options are to increase your hours worked or increase your hourly wage. That “time for money” exchange is exhausting. And you’ll never really get ahead of that game.

But if you have $250,000 in a brokerage account and you earn 10% interest on that money each year, you’re earning $25,000 by letting your money work for you without it costing you any time.

Of course, you don’t have $250,000 just sitting around today. So how do you get to the point where you do?

You start today. Open a Robinhood account or be an old dude like me and start an E-Trade account or something like that…. then transfer $100 into it from your savings account and commit to doing the same every time you get paid.

That’s how you start moving towards having $250,000… $100 at a time and compounding interest.

The Best Investment Advice I’ve Ever Received

So where should you get started? For me, that was the big question. My original 401k offered a group of mutual funds to pick from, it was all so confusing, and I was completely not in charge of that choice– it sucked. So I just picked a few and that was it. I never understood why they did good or bad, I just picked ’em and that was that.

But when I left that job and moved that 401k into an IRA I needed an actual strategy and didn’t know where to look. So I checked an audio book out of the library called, The Motley Fool Investment Guide. (This book has been updated and improved over time, I still recommend it.)

I’ll summarize the entire book with my one takeaway that’s helped me since the late 1990s: Buy stocks from companies you know and love.

Honestly, that’s it. That’s about all I’ve ever done.

I find that I do worse with owning a company’s stock if I don’t really understand how their business works. Maybe you watched a TV show and the guy talked about a stock for 30 seconds and told you BUY, BUY, BUY.

But you really have no idea what that company does, what they are all about, or even how their business actually works. Or worse, you end up buying a complex financial instrument that you totally don’t understand so you don’t know when to get in or get out and get stuck holding the bag on a pump & dump scam. (Cough, DOGE Coin, cough cough.)

I would encourage you to do something simpler. Take your own experience and knowledge of companies you already know and decide if you want to invest in them.

A Tangible Example

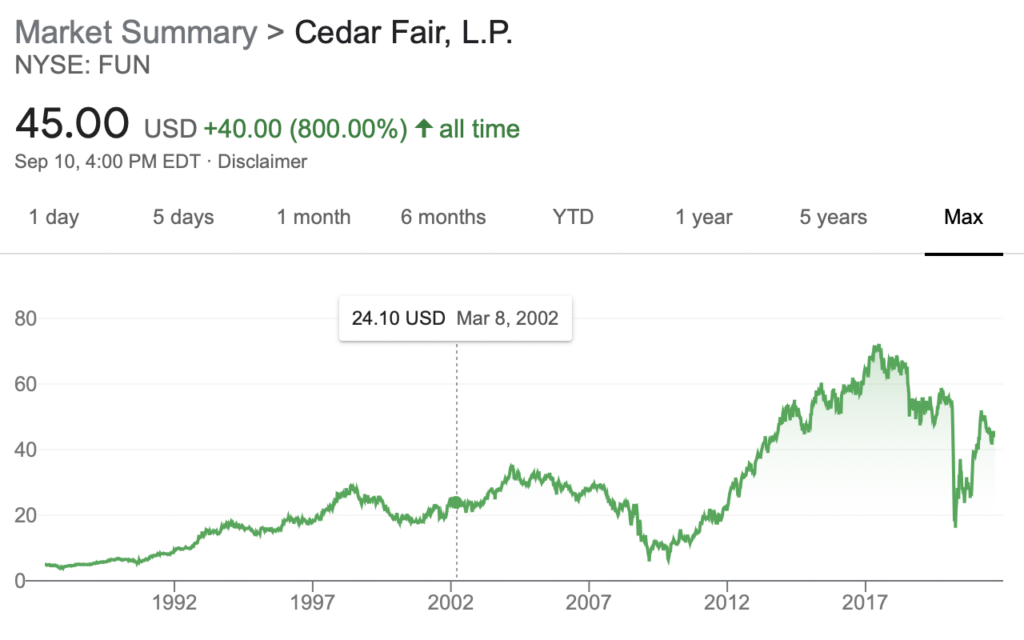

Cedar Fair: (a stock I formerly owned but no longer do.) I grew up in Northern Indiana and as a kid I loved going to Cedar Point. Millions of people in the Midwest are ravenous fans of that place and make the journey to the amusement park each year to see what is new and test themselves against the biggest, baddest roller coasters on the planet. So, when the 2009 meltdown of the stock market hit, I took that knowledge and thought: “Hey… if I’m a parent living in the midwest and there are tough times economically… I might not take that big family vacation to Florida over the next couple of years… but I’ll still want to do something fun with my family… so I bet more people will go to Cedar Point in a recession than would during normal times.”

With that thought I bought as many shares of their parent company, Cedar Fair, as I could. (Stock ticker: FUN) And you know what? I was right. Park attendance and sales went up during the recession and so did their stock value. And when the recession started to recede and families started doing big cruises and vacations in Florida instead… I sold my shares for a healthy profit.

I’ve continued this strategy over the past decade during highs and lows and it’s panned out very well. (I’m no expert, I’m just a dude that pays attention to what I like!)

So, if you are looking for stocks to invest in, spend 20 minutes walking around your house or thinking through your friends and jot down the names of companies/brands you love and have a sense for how their business might operate. The other day I was looking for a new company to invest in and spent a few minutes looking at the apps on my phone to discover two companies I love but hadn’t yet invested in. (DM me for those company names!)

There’s a good chance that a product you buy all the time or a brand you like to associate with or a company your friend works for that is always hiring… that those are good businesses worth investing in to get a solid return on your investment over the long haul.

Bad companies might make a splash and have a big return for a short amount of time. But solid, endearing companies, tend to be profitable for a long, long time.

Keep It Simple, Stupid

Now, once you own those stocks, don’t tune out, instead I find that you’ll naturally start to pay attention to them in a different way.

Let’s say you like to shop at Walmart. (I don’t shop there often and I don’t own Walmart stock, this is just an example.) And you’re there 1-2 times per week. But over time you start to notice yourself not shopping at Walmart as much as you used to and instead you’re going to a local grocery chain… pay attention to that kind of thing because chances are you’re not alone. (Maybe it’s a good time to sell because you don’t know/love it anymore!) Or maybe your friend just got a new gadget that you really want. And at work you hear co-workers saying they are also saving up to buy that same gadget and you’re all kind of lusting for this new, it thing. That’s a stock you’d want to look at because growth is probably on the horizon! Or let’s say your best friend has worked for a company for a long time and they are just ravenous in their love for the company because the management treats them so well. That might be a good company to invest in, right? Good management means good profits and stability. So that’s worth checking out.

It’s much better to buy stocks from companies you love and understand than it is to buy stocks or investments in companies you don’t… even if those companies might seem to perform better. Over the long haul, you’ll do better and you’ll sleep better at night.

Sleep On It

I’ll close with this one last bit of unsolicited investment advice. Don’t react to everything. Sleep on it. Buy and sell on results, not the news of the day. (I actually love bad news for good companies… buy that dip!)

Just because your friend got laid off from that great company doesn’t mean you need to sell today. Or just because Adam said “find a company you love and invest in it” doesn’t mean you need to buy that company’s stock today.

Don’t react. Sleep on it. Make rational decisions.

All of my worst stock owning moments have been the same. I react to the news of the day instead of trusting my gut. So now I have a little rule: Sleep on it. If I still want to make that move the next day, then I do it. But I don’t like waking up on a Monday morning, checking my portfolio, and reacting. That’s when I make big mistakes and lose money.

Questions: Drop me a comment or send me a message on your favorite social platform.

Leave a Reply